I usually publish one article per day, but this is a special case: I have five meetings today and need to leave soon, so I wanted to get this out to members before the market closed.

Why I’m Selling Alexandria Real Estate (The Facts Changed So I Changed My Mind)

Alexandria Real Estate is one of the ZEUS stocks, and during its earnings call, it cut 2025 guidance by 3%. However, it was the following that triggered this nearly 30% (at one point) crash.

Here is the big reason for the collapse.

“in light of market and life science industry conditions and our continued focus on capital efficiency, our Board of Directors expects to carefully evaluate our 2026 dividend strategy.”

The company has an annual investor presentation in December; however, the stock’s reaction, driving the yield to as high as 9.5% at one point, implies a potential 30% to 40% dividend cut (which would return the dividend yield to pre-crash levels).

What does the FactSet consensus (median of all 15 analysts covering ARE) say?

Note the 2026 FFO/share consensus was $8.29, which was already a 10% YOY decline.

No dividend cut is currently expected (just a one-year freeze), BUT then the company announced the following.

The FFO/share guidance of $6.55 midrange (and the 10% range) is rather extreme, as it represents a 21% decline from analyst estimates.

While the 81% AFFO payout ratio consensus for 2026 and 2027 is manageable… that was before FFO declined by 21%, which could mean a 23% decline in AFFO.

That would push the AFFO payout ratio to 104% the highest in the REIT’s history.

During the GFC, the payout ratio peaked at 62% before management cut the dividend…twice.

In fact, the payout ratio was only 58% in the GFC before management cut the dividend 17% the first time, and then 35% the 2nd time (when the payout ratio was just 61%).

Alexandria Real Estate Safety Update Monday Night (Earnings Night)

I recall a member asking me about ARE on Tuesday morning, before the conference call, and I explained that the risk of the thesis breaking was real, but the thesis was intact because of the analysis above.

Then on Tuesday, the conference call came out, and ARE fell another 6%, and the 8K came out.

I loaded the 10Q and 8K and conference call transcript into Chat GPT 5 Pro (who uses the master prompt and my carefully curated data from FactSet, GuruFocus, Morningstar, S&P, FAST Graphs, ect) to analyze companies using our 77-page safety and quality system (generation 4).

And here were the Tuesday results.

Alexandria Real Estate Safety Update Tuesday

And finally, this morning, after adding all the additional analyst notes that FactSet has available and factoring in the potential for AFFO to come in $4.91 to $5.01 (based on management guidance), I had ChatGPT 5 Pro update the safety and quality model one final time.

And right now, here’s how things stand for Alexandria.

Alexandria Real Estate Post Earnings Safety & Quality Update

Our model is now estimating an 80% risk of a dividend cut in the next year, based on the 23% AFFO guidance cut management just announced (extrapolated from the 21% FFO guidance cut).

Historically, when REITs have faced 107% AFFO payout ratios in similar circumstances, 80% of them have cut dividends.

ARE is now the 4th-lowest-quality company on the Master List and the most likely to cut its dividend in the next year (by far).

I am selling my ARE at a 17% realized loss, which is the largest % loss I’ve ever taken in ZEUS.

Long-time members will know I have a very clear rule about dividend cutters.

When the dividend is cut it’s time To Sell

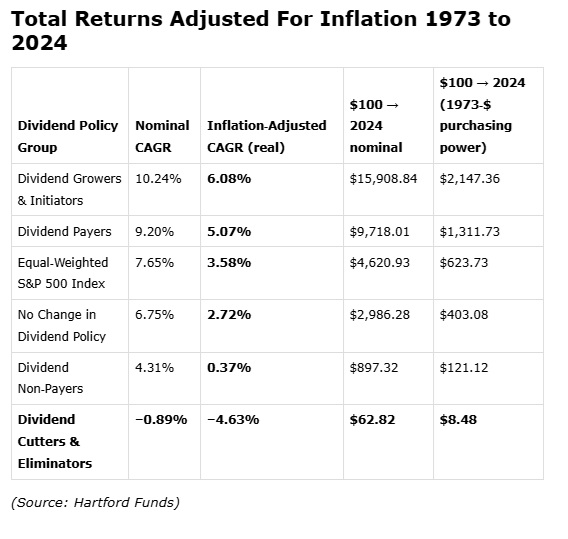

Historically, 91% inflation-adjusted total returns from buying and holding dividend cutters for 50 years is enough for me to say that if the dividend is cut, it’s time to move on. In this case? The data says 80% chance of a cut.

Those are overwhelming odds, which, for me, Connor, and my family specifically (more on this on Monday), means we can’t hold on hoping that a 20% probability comes through and makes ARE into a potential 3X return in 5 years.

Context Makes All The Difference

ARE Is The First double-digit % Loser In ZEUS (Out Of 39 Trades). 79% of Realized Trades Are Profitable So Far

I’ll explain more in the Monday Special Report about the ZEUS portfolio, which would have come out over a week ago, BUT due to all the chaos and work that went into launching GNG, I wasn’t able to.

The essence of disciplined financial science is that you can never fall in love with a stock, and when the facts change, you change your mind as fast as possible, making reasonable, fact-based (not emotional) decisions.

That’s how I delivered 20% total returns (including dividends) on 30% of my 3,600 recommendations during my 10 years at Seeking Alpha.

Not because our models are perfect, but because we are rules-based investors, fundamental quants, and there is no ego…ever.

Everyone who is following our tools, our recommendations, and my family and friends’ future riding on the ZEUS fund (17 people and counting) requires my facts and reasoning to be right.

So when the facts change? I change my mind, and if it turns out that, in hindsight, I made a mistake? Well, as Peter Lynch said, "If you’re good, you’re right six times out of ten. You’ll never be right nine times out of ten.”

So far, ZEUS has been right 80% of the time on realized trades. The only way I’ll be able to sustain anything close to those statistics is by working with Connor, and future team members (and all of you and your fantastic ideas🤗 to ensure that our facts and reasoning are as correct as possible.

And when we are wrong? As long as you’re a disciplined financial scientist, you’re never mistaken for long. 😉

Alexandria Real Estate PEGY Analysis

The consensus growth rate has yet to change to update the $6.51 mid-range 2026 FFO guidance, so take the 4.8% 2026-2028 growth recovery with a grain of salt.

If it eventually returns to the historical growth of 5%, then today’s 9% yield implies long-term returns of 14% to 15% (plus the valuation boost).

BUT remember that this requires the dividend NOT TO BE CUT—a 20% probability based on the new best data we have.

That means the most likely long-term return for ARE (if it grows at only 2%) is 6% yield + 2% growth = 8% to 9% historical total returns.

In other words, if the growth rebound isn’t realized, ARE is “cheap for a reason”.

Not a value trap (post dividend cut), but simply not an undervalued company.

However, the turnaround for ARE has been continually pushed back. Given the stresses in the biotech industry over the next few years (the MAHA movement means much more regulatory scrutiny), it might be a long time before ARE actually achieves that turnaround.

For now, it looks like the stock is pricing in 2% growth, not 5%, and if that proves true, the long-term returns would be 11%, with no valuation boost, since the stock is currently fairly priced for 2% growth.